We attended AHOU in Austin earlier this month – the premier annual gathering for life insurance underwriters, actuaries, and risk executives. Across many carrier and platform meetings, a consistent picture emerged: the industry is expanding its appetite for digital, accelerated underwriting at exactly the moment its risk visibility is shrinking.

Forces reshaping life insurance underwriting

The self-attestation gap is a known problem with no good solution yet

Carrier after carrier described the same scenario: an applicant self-attests to no criminal history, the current vendor runs a check, nothing comes back—not because the applicant is clean, but because the coverage is incomplete. In certain states, hit rates are so low that carriers are effectively relying on the honor system. Applicants who omit criminal history, DUIs, or serious driving violations represent elevated mortality risk that goes unpriced at underwriting and surfaces later in claims. The risk signals you miss at underwriting become the claims you pay later.

Current data is arriving at the wrong point in the funnel

Most carriers run criminal and driving checks late in the customer journey — after significant cost has already been invested in the applicant. Per-transaction pricing creates a structural disincentive to screen earlier. What carriers haven’t had access to is a model that decouples data spend from applicant volume: one where early-funnel screening costs nothing unless a policy closes.

Trends across life insurance underwriting

1. Behavioral and criminal data is being taken seriously as a mortality signal

The actuarial case is clear. Applicants with serious driving violations carry a significantly higher mortality risk. Combining motor vehicle records with court records uncovers double-digit percentage point increases in violations compared to either source alone. Criminal history, driving records, and civil data are moving from compliance considerations to underwriting inputs — and the carriers furthest along are building them into automated decisioning rules.

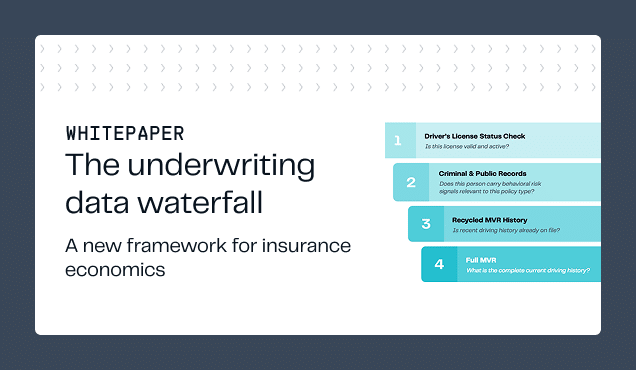

2. Driver’s license status is an underused pre-screening signal

Before pulling a full MVR, confirming that a license is valid and active filters out a meaningful segment of high-risk applicants at a fraction of the cost. Carriers currently paying an average of $11 on every MVR, whether or not the applicant ever binds, immediately see the economics of a staged approach: run the cheap signal first, pull the expensive record only when warranted.

3. Platforms and reinsurers are the real distribution layer

The most important data relationships in life insurance underwriting aren’t always direct-to-carrier. Platforms that orchestrate underwriting workflows and reinsurers that set data requirements often control what gets integrated and when. A carrier that has handed off workflow management to a platform partner doesn’t make independent data decisions. Getting into the workflow layer—and aligning with reinsurer expectations—is as important as winning the direct carrier relationship.

Where life insurance underwriting is headed

Instant criminal screening moves to the top of funnel

When a criminal history check returns in sub-seconds, it stops being a downstream verification step and becomes a real-time decisioning input. Carriers that make this shift stop treating behavioral risk as a post-issue audit problem and start treating it as a pre-bind underwriting advantage.

Per-bind pricing becomes the standard

Per-transaction pricing was designed for a world where carriers controlled application volume carefully. In a world of digital acquisition and high quote-to-bind attrition, it creates the wrong incentives — pushing screening later to contain costs. Per-bind pricing removes that constraint and lets carriers screen earlier without data spend scaling against them.

Coverage parity becomes a baseline requirement

The carriers most actively evaluating new data relationships name the same gap first: depth of coverage in the states and counties where their applicants actually live. The next generation of life insurance underwriting data needs to treat broad national coverage as the baseline, not the premium tier.

Checkr Trust is the source of truth for public records, criminal history, and driving data — with broader coverage than legacy providers and a per-bind pricing model built for the way life insurance actually works. Book a meeting to run a structured retrospective study against your existing policy data and see what your current underwriting stack is missing.