We joined auto insurance leaders in for the 2026 Auto Insurance Report National Conference in Dana Point. Across conversations with various carriers, we gleaned a few consistent themes: MVR costs are unsustainable, the data infrastructure underneath underwriting is showing its age, and the industry is actively evaluating what comes next.

Forces reshaping auto insurance underwriting

MVR economics are structurally broken

Motor Vehicle Records remain central to auto insurance underwriting. They’re also the most expensive recurring line item in the data stack. At roughly $11 per pull—a state pass-through fee absorbed entirely by the carrier—the unit economics are difficult at scale.

The cost structure is self-reinforcing. As carriers reduce MVR order volumes to manage spend, states raise per-pull fees to offset declining revenue. Higher fees push more carriers to cut volume further.

Shopping rates are compressing margins

The 47% annual shopping rate recorded in 2025 is an all-time high. That means nearly half of all policyholders are generating new quote activity every year. Combined with 188 million annual quote instances, carriers are running data costs on a volume of applicants that far exceeds their eventual book of business. The gap between data spend and policy yield is widening.

Pre-screening has matured—but the model hasn’t

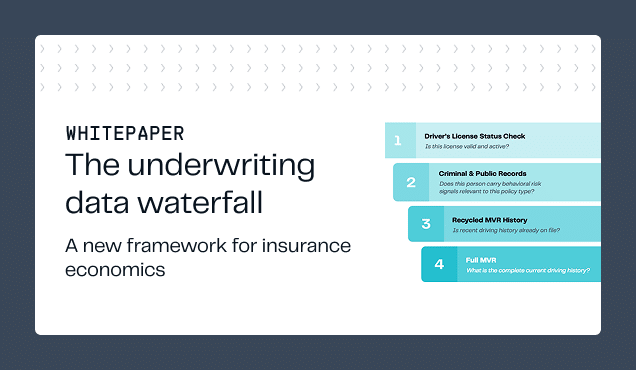

An estimated 90% of carriers now run a criminal or public record check before ordering a full MVR, filtering out high-risk applicants early to avoid pulling expensive records on quotes unlikely to convert. The pre-screening approach has become standard practice. What hasn’t kept pace is the pricing model around it. Most carriers are still paying per-transaction fees on every applicant who enters the funnel, whether or not they close.

Trends reshaping auto insurance underwriting data

1. Coverage gaps are a constraint, not an edge case

Multiple regional carriers— particularly in the Midwest—described meaningful gaps in the criminal and public record data available to them. In some states, the data they need for pre-screening simply isn’t accessible through their current provider. This isn’t a niche problem. For carriers operating outside major coastal markets, incomplete coverage is a baseline limitation that directly affects underwriting quality and risk selection.

2. Signal extraction matters more than signal volume

Carriers consistently said they have more data than they can operationalize. An estimated 90% of insurance data teams reported challenges extracting meaningful risk signals from data already in their workflows. The industry needs a better way to derive value from the data it has—cleaner identity resolution, more actionable scoring, and tighter integration into decisioning workflows.

3. Carriers want pricing aligned with outcomes

The per-transaction pricing model that dominates the market creates a structural misalignment. Carriers pay data costs on every quote, but only earn revenue on policies that close. As shopping rates increase and funnel volumes grow, data spend scales linearly while conversion remains flat. Carriers are looking for models that tie cost to outcomes—specifically, per-closed-policy pricing that aligns data spend with actual premium earned.

4. Partnership quality is becoming a differentiator

A recurring theme across conversations wasn’t about data at all—it was about the vendor relationship. Carriers want data partners who are proactive, responsive, and willing to collaborate on pricing and product. The bar has moved beyond delivering a product that works. Carriers are evaluating whether their data providers operate as strategic partners or transactional vendors, and they’re making decisions accordingly.

Where the underwriting data stack is headed

The conference reinforced a thesis that’s been building across the industry: the next evolution of the auto insurance data stack isn’t about inventing new data types. It’s about restructuring how existing data is priced, delivered, and integrated into carrier workflows.

Three shifts are likely to define the next cycle:

Per-closed-policy pricing becomes the standard

The economic logic is straightforward. When data cost is tied to closed policies rather than quote volume, carriers can expand top-of-funnel acquisition without proportionally increasing data spend. This aligns vendor incentives with carrier outcomes and removes the structural tension between marketing investment and data cost. The carriers who adopt this model first will have a meaningful cost advantage as shopping rates continue to rise.

Coverage parity across all 50 states becomes a requirement

As carriers expand into underserved regions or write national books, they need consistent data infrastructure across every state. Coverage gaps that were tolerable when a carrier operated regionally become critical when the book grows. The expectation is moving toward full nationwide coverage for criminal, public record, and MVR data as a baseline, not a premium tier.

Autonomous vehicle underwriting creates a new data layer

An emerging question surfaced repeatedly at the conference: how should carriers underwrite hybrid risk for vehicles that increasingly drive themselves? Traditional MVR-based risk models assume a human driver. As AV technology enters the fleet, carriers need risk signals that account for both human and machine behavior. The underwriting data infrastructure to support this doesn’t exist yet—and the carriers asking the question today will shape how it gets built.

Checkr Trust works directly with auto insurance carriers on coverage, MVR cost reduction, and outcome-aligned pricing models. Talk to our team to audit your MVR costs and reevaluate your underwriting data stack.